Telstra versus the Government

The war of words between Telstra, the government and the competition regulator has perplexed and frustrated investors and observers.

It started soon after the appointment of Sol Trujillo last July and continued well into this year. Telstra and the regulator are now talking but the dispute is not settled.

What seems obvious is that Telstra has been playing some form of game with the government. The question is: what kind of game? And, more importantly, has Telstra been winning or losing?

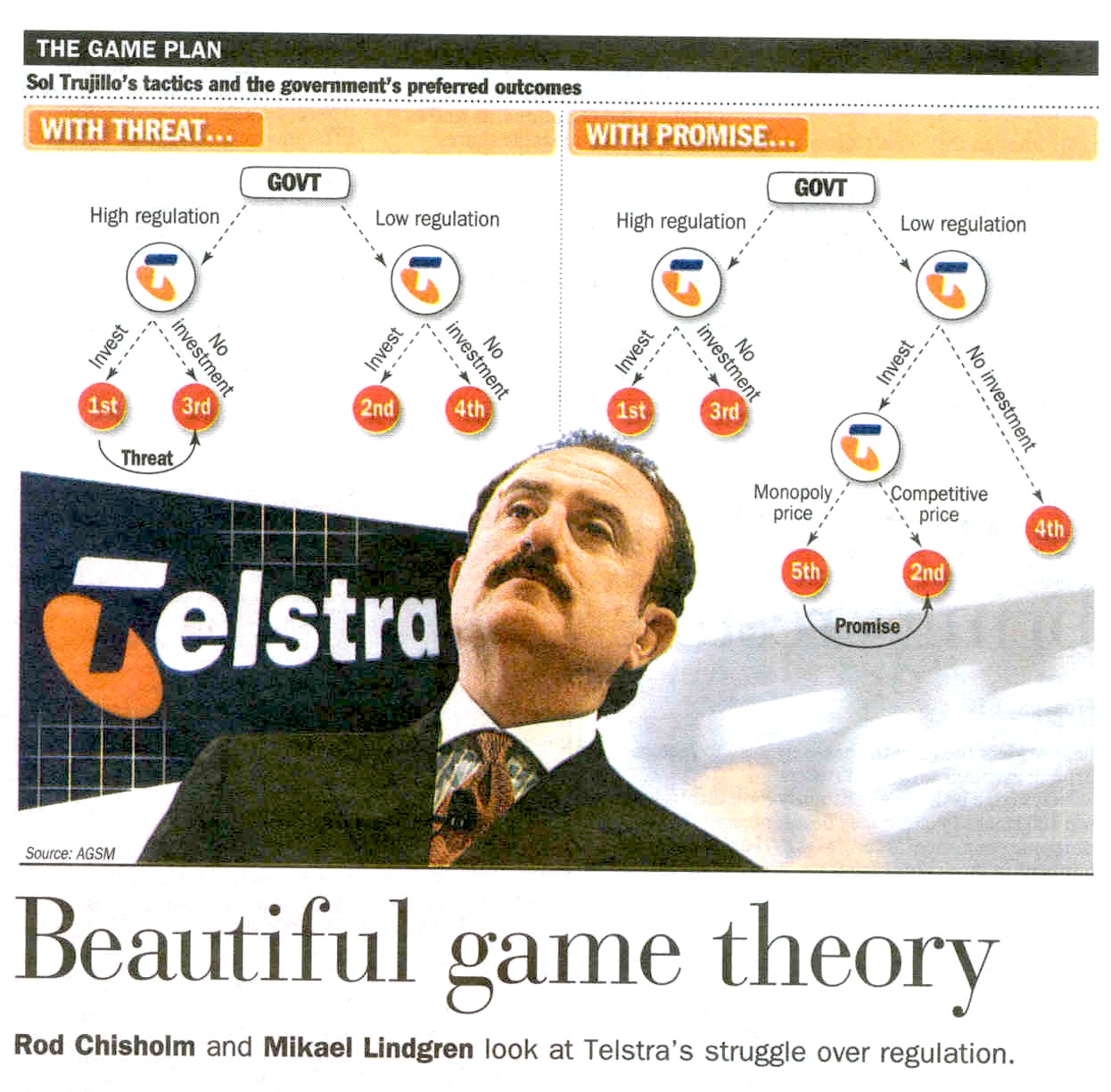

The basic moves of the game have been simple. The government had to decide how to regulate Telstra. Telstra then had to decide how much to invest in advanced telecommunications services.

The government wanted to see investment in new services without a reduction in regulation. Telstra wanted a reduction in regulation before investing in new services.

So who would get their way? This is where the science of game theory (developed by John Nash and made famous by the film A Beautiful Mind) can provide answers.

The government would make its best decision by anticipating Telstra's best response (looking forwards and reasoning backwards). Telstra's choice is between investing and not investing, given the regulatory decision by the government.

The problem for Telstra was always that the government clearly believed (and our own estimates confirm) that it was always better for Telstra to invest rather than not invest, irrespective of the regulatory decision.

So the prediction of game theory was that the government would choose its preferred move -- no reduction in regulation -- and Telstra would choose its best response: investment. The government would get its way.

Faced with a losing position, Telstra attempted to change the outcome. In order to achieve this, Telstra had to convince the government that it would not invest under high regulation. This would reduce the government's payoff from high regulation and cause it to choose low regulation instead.

Telstra attempted to convince the government by issuing a series of threats that amounted to a commitment to act against its own interests to inflict damage on the government.

The threat was articulated clearly in its November 15 briefings: if Telstra did not get a break on regulation, there would be no new network.

But talk is cheap. To work, threats must be credible. There had to be some penalty for Telstra if it did not carry out the threat, or else the government would quite rightly ignore it. Thus Telstra started making its announcements through the Australian Stock Exchange, where there are more serious consequences to making misleading statements.

Another way to change the outcome is to change the payoffs for the other party. By continuously directly linking regulatory outcomes to financial performance, Telstra tried to make the government's regulatory decision a financial move rather than a policy move.

Our estimates and Telstra's guidance indicate that the government's decision on regulation could alter its proceeds from the T3 share sale by as much as $8 billion.

Have Telstra's threats succeeded in significantly changing the regulatory regime? At this point, the signs are negative.

Having chosen to go down the route of threats, Telstra ran the risk that its bluff would be called. This is the drawback to using threats: to follow through destroys shareholder value and to renege destroys management's credibility.

But there was always a way out of what seemed a lose-lose situation. In game theory you do not always need threats to get your way: sometimes all that is needed is to examine in more detail the game you are playing.

The Telstra game plan assumed that the government was opposed to low regulation in principle. But we would argue that governments, in general, are ambivalent about regulation. What governments are afraid of is allowing an ex-public utility such as Telstra to act like a monopoly, stifling competition and charging monopoly prices.

Monopoly pricing is an option under reduced regulation. But it is not the only option. Telstra could choose to set competitive prices and not to use its regulatory break to force competitors out of the market.

This is a potential win-win situation for both the government and Telstra.

The key that unlocks this opportunity is a credible promise from Telstra to price competitively under low regulation. If the government believes that Telstra would not abuse low regulation with monopoly prices, then this becomes its favoured outcome.

This is not a new or unique idea. There is international precedence from the Scandinavian telecommunications markets, where low prices and advanced infrastructure have developed without resorting to harsh regulation.

This type of outcome, however, requires a new level of trust between the government and Telstra.

As Telstra continued to raise the stakes with its threats, the game looked destined for a lose-lose rather than a win-win solution.

Telstra needed to stop fighting like Russell Crowe in Gladiator and start thinking more like John Nash.

-- The Australian Financial Review, 19 June, 2006, p.24.

Up

Last Updated 10 July, 2006 Robert Marks, bobm@agsm.edu.au